UK Election Result

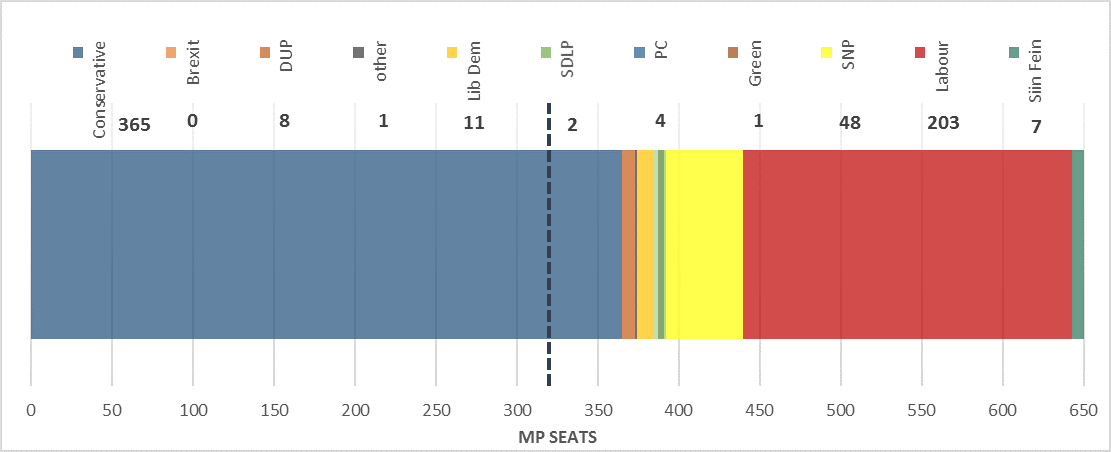

The result of the UK Election of 12th December is projected as follows, with just 1 seat left to declare:

The Conservative party achieved an unexpected landslide victory with 365 seats and a huge majority of 78. This is a remarkable result for Boris Johnson and the worst performance from the Labour party since 1935, only just scraping over the 200 seat mark. The Liberal Democrats also suffered. Despite increasing their overall share of the vote, they were squeezed out in 10 seats, including that of their leader Jo Swinson, leaving them with just 11. The Scottish National Party by contrast performed well gaining 13 seats to take their total to 48.

If a Conservative majority was expected, the scale of it and the implications for the economy has been greatly underestimated. The UK has perhaps forgotten what it means to have a strong government and certainly a strong Conservative majority. The Conservatives have actually only enjoyed a (thin) majority in the House of Commons for 2 out of the past 22 years, following David Cameron’s victory in 2015. The last time the Conservatives achieved a strong majority was as far back as Mrs Thatcher’s 3rd term in 1987.

For over a decade the UK has endured weak government and more recently a parliament in deadlock with the growing threat of an extreme left-wing opposition led by Corbyn’s Labour party and the Scottish National Party. This election presented the very real prospect of a seismic shift from free-market economics to escalating state control with a wave of nationalisations, share confiscations, board appointments, massive borrowing and a step change in taxation. Add to this the turbulence and uncertainty of Brexit and it is hardly surprising that business investment slowed to a trickle this year as business and consumer confidence fell. This in turn led to weak economic growth and a market wary of Sterling and UK assets.

The good news is that business investment, for the most part, has only been delayed and UK assets are cheap relative to other major markets. Regardless of one’s political perspective, this Conservative election victory settles the political uncertainty for at least 5 years and in doing so we believe enables business investment and confidence to accelerate rapidly, lifting the UK economy and attracting investors back to the Pound and UK markets.

There remain substantial challenges. Most notably agreeing the future relationship with the EU, managing the debt bubble and the SNP’s growing demand for a 2nd independence referendum in Scotland. Perhaps the greatest challenge is to bring the country back together and address the relative stagnation and rising inequality of the last decade that led to the Corbyn threat. With a strong government that work can at least now begin in earnest and, in our view, the UK is now likely to enter a relatively positive ‘purple patch’ with calmer seas and a brisk following wind.

At heart, Boris Johnson is a liberal conservative and a pragmatist. With such a substantial majority, the Prime Minister can now set his own agenda. We anticipate he will want to agree the future relationship with Europe as rapidly as possible and get back onto the domestic agenda. To do so we expect him to opt for a soft free trade agreement (FTA) with relatively close alignment to the EU. This may surprise many but will simplify the negotiation process dramatically while leaving open the option of greater divergence in the future. This may limit the scope of trade agreements with the rest of the world, at least in the near term, but does not preclude them.

The SNP’s success in Scotland will lead to increasingly loud demands for a 2nd independence referendum. In practice, however, Nicola Sturgeon may only have a window of 2-3 years during which support for a 2nd referendum remains favourable. Thereafter, Boris Johnson will hope that the much hyped Brexit ‘catastrophe’ proves to be no more than a ripple, the UK economy rebounds and he can make progress with his domestic agenda. We can expect significant infrastructure spending and a charm offensive across Scotland to boost the all-important feel good factor. At the same time the SNP will be defending their difficult record after well over a decade in power. The Prime Minister may judge that all he has to do is wait and the issue will fade ahead of the next election.

From a market perspective there has been significant volatility in the lead up to the general election as the risks on both sides have weighted heavily on investor minds. During such periods of heighted volatility it is critically important that investors keep well-grounded in the longer term view, so as to avoid getting caught out by sudden market movements. We believe the outlook has turned decidedly more positive for the UK and we expect a period of catch-up for domestic UK equities and in the value of Sterling.

Our investment strategies were positioned for a Conservative victory and the anticipated positive market response. In preparation for the possibility of an alternative outcome, we had pre-programmed a range of trades and the investment and dealing departments were manned and ready to be able to react through the night, had the election taken a different turn. I am pleased to say that such action was not necessary and our strategies have responded well to events.

With election fever at last behind us I am delighted to be able to wish you all a very happy Christmas and prosperous New Year.

Disclaimer: The views thoughts and opinions expressed within this article are those of the author, and not those of any company within the Capital International Group (CIG) and as such are neither given nor endorsed by CIG. Information in this article does not constitute investment advice or an offer or an invitation by or on behalf of any company within the Capital International Group of companies to buy or sell any product or security.