COVID-19: Reaching The Peak

Financial markets have improved markedly over the past 10 days or so as hopes have grown that Europe may be passing through the peak of the COVID-19 pandemic.

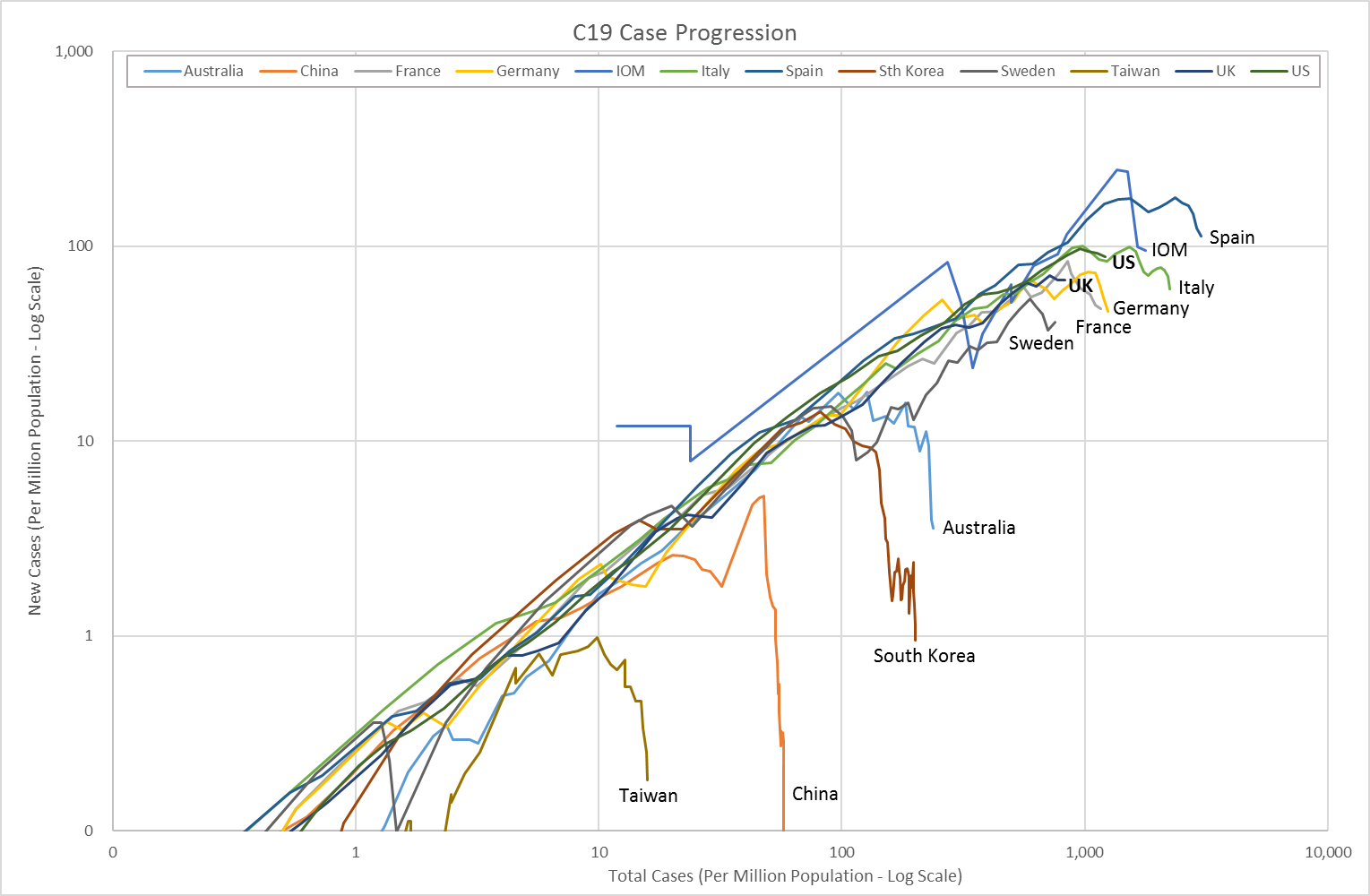

Our own analysis shows this clearly, as illustrated in the chart below. Case progression across countries is shown on a standardised basis per million of population, using log scales.

Left to its own devices, COVID-19 would progress exponentially, at least until much of the population had been infected. On this chart an exponential progression would appear as a 45 degree straight line, and one can clearly see that all countries have followed this exponential path initially.

The important point to note from the chart is when countries start to fall away from the 45 degree line; the first to do so was China where the outbreak began, although it is likely that the data out of China grossly under-reported the true number of cases. The shape of China’s chart would be the same but its position should be somewhere between Australia and Sweden, perhaps as much as 20-40 times the official numbers.

Had the world fully appreciated this at an early stage, it is possible that countries would have moved faster to contain the outbreak. Asian countries that had experienced the outbreaks of bird flu in the ‘90s and SARS in 2002 such as Taiwan, Singapore and South Korea acted swiftly to introduce containment measures. The impact of this is clear from the chart, with Taiwan in particular stopping the outbreak almost immediately.

Further afield in Europe and North America a slower response allowed the outbreak to grow exponentially for far longer, necessitating a much more severe lockdown of activity to turn the tide. However, those measures are starting to work. All European countries have started to drop away from the exponential line, as illustrated above, but we are not able to relax yet. If the lock down measures can be maintained for a couple more weeks, there is reason to hope that new case rates in Europe will start to fall rapidly and their charts will start to resemble China’s or Australia’s.

We need to see the new case rate fall to an average of below 10 new cases per million of population per day to get COVID-19 back under control, and this is possible within the next month even in the USA which is about two weeks behind Italy.

This is very good news, but the margin for error is now very small. Millions of businesses have been forced to press the pause button. It’s as if the oxygen has been sucked out of the economy. Those businesses with reserves can hold their breath long enough to bounce back, but millions of small enterprises are now in real trouble. Every day the lock down continues, more will fail and more jobs will be lost.

The urgency now to get the economy moving again cannot be underestimated, but the timing is critical – too early and we risk a second wave, too late and the economic damage will be too great to simply bounce back from, no matter how great the stimulus package.

At this stage, politicians are rightly focused on containing the outbreak; with the media counting every casualty, this is understandable. However, the debate needs to begin focussing now on how to restart the global economy as soon as possible and avoid a recessionary spiral that will cost far more lives in the longer term.

There are other reasons to be optimistic. It is encouraging to see China relaxing restrictions in Wuhan and starting to get the country back to work. There is also growing confidence that some treatments are helping, most notably the use of convalescent plasma therapy, which was the most common way in which viruses were treated before vaccines became widespread.

Interesting evidence is also building to suggest that the proportion of very mild or asymptomatic cases of infection is much higher than previously thought with testing of cruise ship passengers, survey data in Italy and current testing in China suggesting asymptomatic cases may be somewhere between 30-70% of all cases. If true, this would suggest the outbreak has already spread far wider than previously estimated with the positive implication that the mortality rate is much lower than currently understood.

From a market perspective we believe the news-flow is likely to remain fairly positive and supportive of a continued recovery in markets at least until the Q1 earnings season in about 10 days, when we will see the true impact on corporate earnings for the first time. Expectations are already extremely low, but it is likely we will see some truly shocking earnings reports and guidance for the remainder of the year. This reality check could easily see the lows re-tested, so we must remain relatively cautious of pursuing the current rally too far.

Finally, while one individual may be irrelevant in the context of this pandemic, the news that Boris Johnson, the UK Prime Minister, was moved to an intensive care unit on Monday is a stark reminder of the very real human tragedy that is unfolding. It is easy to analyse the statistics and forget the human cost, which is touching so many.

We wish the Prime Minister a speedy recovery as we do all who are battling this dreadful disease.

Disclaimer: The views thoughts and opinions expressed within this article are those of the author, and not those of any company within the Capital International Group (CIG) and as such are neither given nor endorsed by CIG. Information in this article does not constitute investment advice or an offer or an invitation by or on behalf of any company within the Capital International Group of companies to buy or sell any product or security.