A Changing World: Debt, Debasement and the Race for Productivity

We are living through a period that feels increasingly chaotic but beneath the noise of headlines and political volatility, there are deeper structural forces shaping the global economy, forces that will define investment returns and economic outcomes for years to come.

Geopolitics is often treated as the starting point for economic change. In reality, it is usually the consequence. Since the end of World War II, the rules-based order has been anchored by US industrial and financial dominance, held together by the US dollar as the world’s reserve currency and US Treasuries as the global reserve asset.

As that system comes under strain, cooperation gives way to competition, rules give way to power, and the global landscape begins to look less exceptional and more historically normal.

To understand what comes next, it helps to focus on two defining forces: the constraint and the engine.

The Constraint: A World Drowning in Debt

The global economy is burdened by an unprecedented level of debt. This is not a moral judgement; it is a mathematical one. Global debt is estimated at roughly two and a half times global GDP. At this scale, it cannot realistically be “paid down” in the normal way.

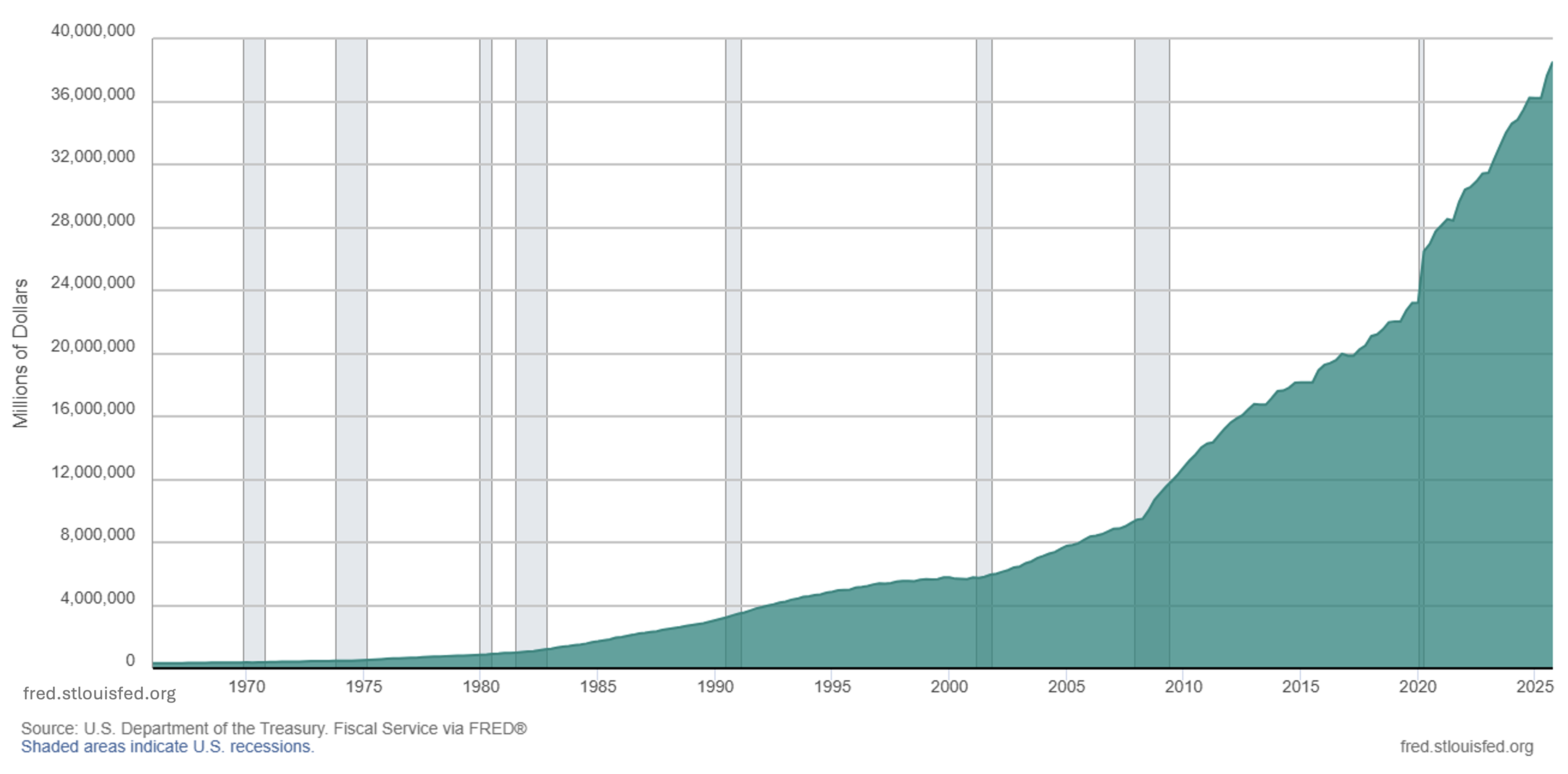

The United States sits at the centre of this dynamic. Its debt continues to rise at a remarkable pace. In just one year, the US has added about 3 trillion dollars of debt, taking the total to roughly 39 trillion. The interest bill alone is approaching one and a quarter trillion dollars (roughly 3 times the size of the entire South African economy) just in interest.

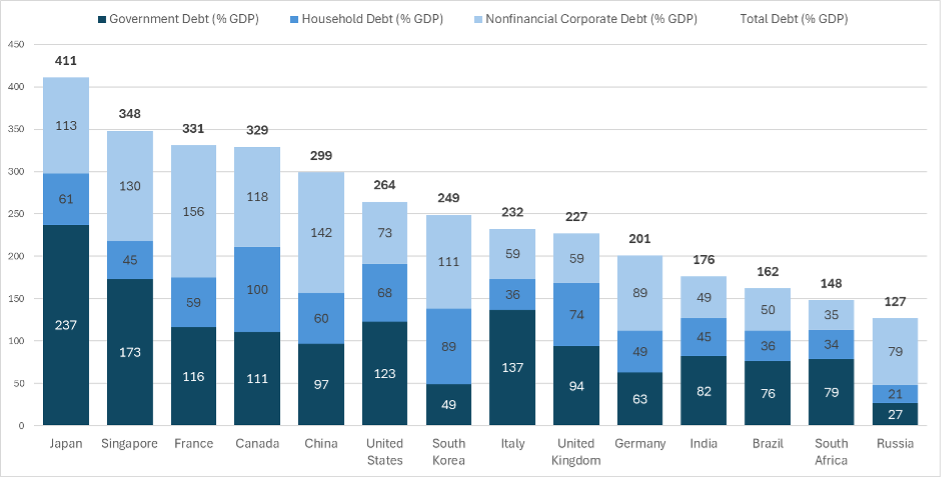

This is not just an American issue. Across much of the developed world, governments, households, and corporations are more leveraged than at almost any time in modern history. Importantly, much of this debt was accumulated during a period of unusually low interest rates and highly supportive financial conditions. That matters because it means this is not debt that can easily be grown out of.

For the past two decades, using ever more debt to stimulate growth has been the norm. Increasingly now, debt itself is becoming the constraint.

The Tipping Point

Borrowing may have become normalised but there is a limit, where the rising cost of debt becomes inescapable. Then, there are only four ways out: austerity, taxes, growth, or inflation. History tells us which option tends to be chosen.

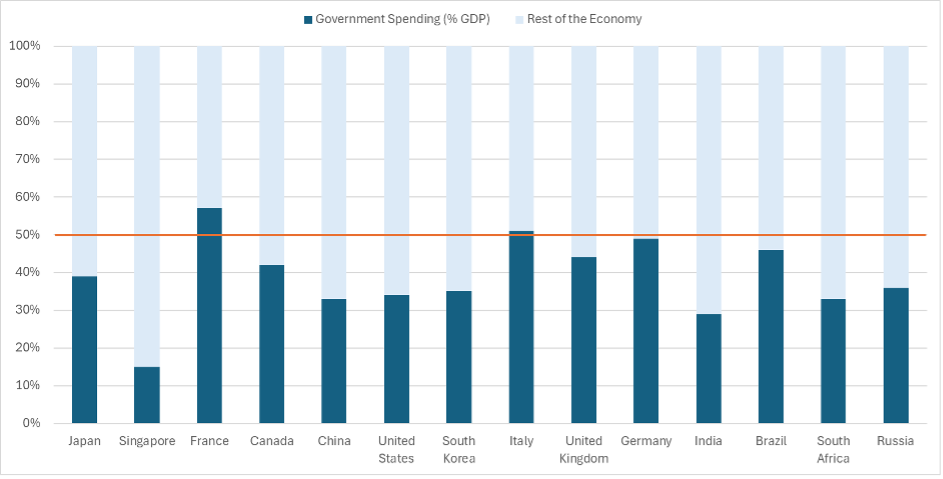

The root of the problem, of course, is the persistent growth in public spending that has expanded faster than the political appetite to pay for it. On this metric, the US is actually positioned better than many with public spending at 34% of GDP.

Public spending in much of Europe is approaching or even exceeding 50% of GDP such as in France, Italy and even Germany. From these levels, the scale of austerity required to balance the books has become politically unimaginable.

Even where there is capacity for governments to reduce the deficit purely through taxation, this too is politically very challenging. Both austerity and increased taxation have a direct and immediate impact on living standards. So in practice, policymakers seek another way out.

In broad terms, there are two paths:

Path A is the textbook. Fiscal discipline, monetary restraint, lower inflation and stronger real growth that lifts living standards. But fiscal discipline is painful and achieving real economic growth simply cannot be engineered at the command of any government.

So, Path B becomes the politically expedient option. Tolerate higher inflation, run larger deficits, and prioritise nominal growth over balance sheet repair.

Policy makers everywhere have chosen some version of Path B. This is not an accidental mistake, it is a rational policy choice and broadly, we must expect this policy to continue.

Debasement: The Hidden Tax

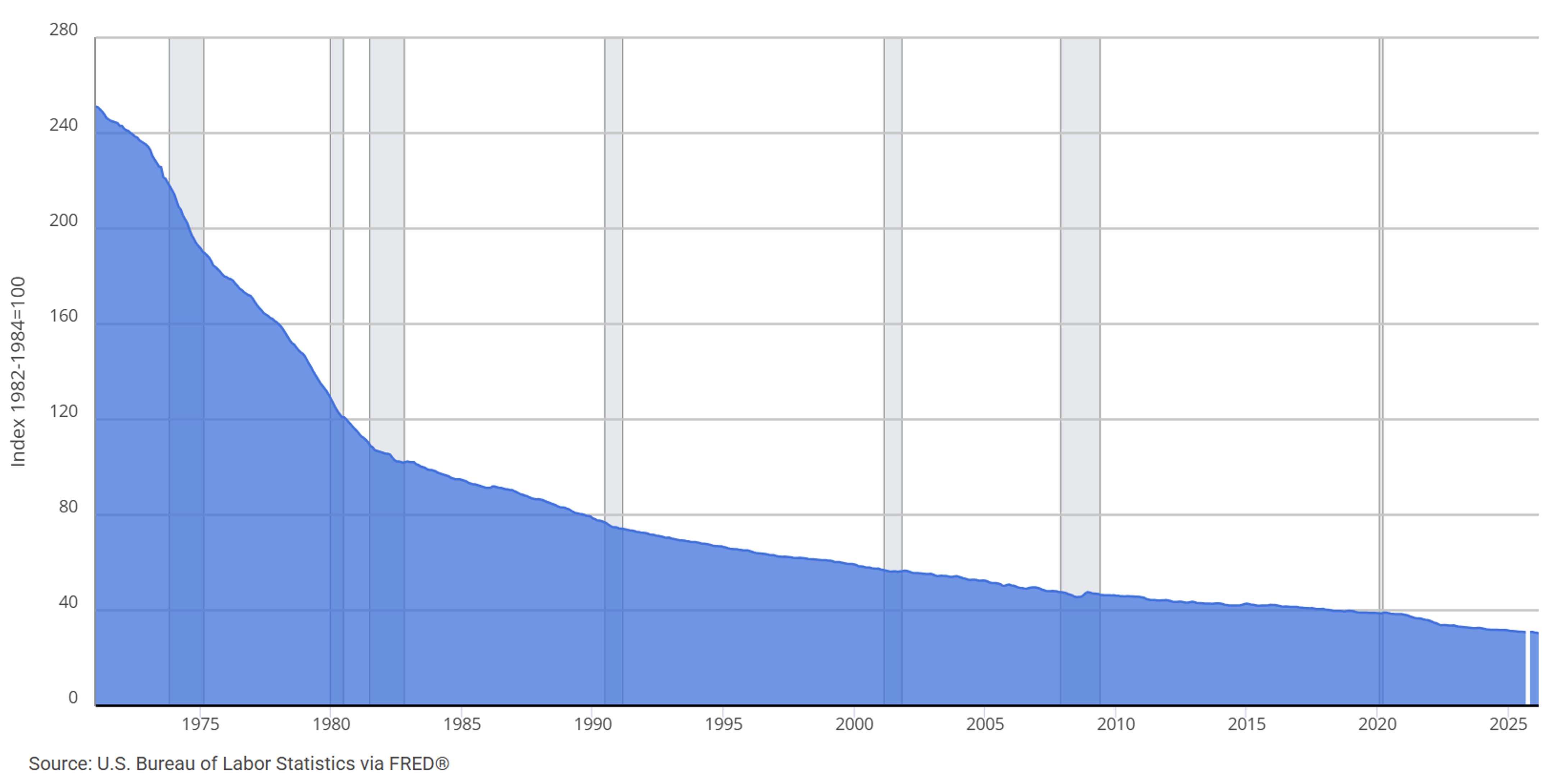

Inflation in the context of Path B acts as a hidden tax, gradually eroding purchasing power over time, a process that can be described as debasement.

Over the past few decades, inflation has significantly reduced the real value of money. While nominal incomes and asset prices may rise, real purchasing power declines. Year after year, nominal values drift higher, while the real value of money quietly erodes. For investors, this reframes the central question. It is not about whether a currency will collapse. Major currencies face similar structural pressures. The more relevant question is: What actually preserves purchasing power?

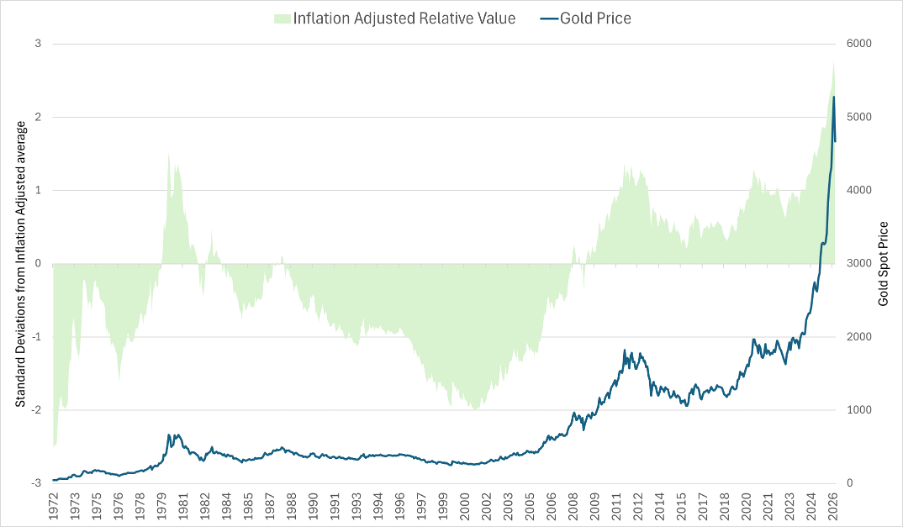

Is Gold the Answer?

In an environment of persistent debasement, assets that hold value over time become increasingly important. Gold has historically played this role, acting as a store of value and a form of insurance.

However, gold is not a complete solution. It generates no income, has limited productive use, and cannot function as a modern monetary system. Over the long term, productive assets, businesses that innovate, reinvest, and grow should still outperform. At the same time, the current environment is unusual: almost everything looks expensive.

Equities, property, and real assets are all trading at elevated levels. In a world of abundant liquidity, traditional valuation benchmarks become less reliable. As long as liquidity continues to flow, prices can remain high. But this creates a paradox. The same conditions that drive strong returns also increase systemic fragility. Over time, risks build beneath the surface until, often suddenly, they become visible.

The Engine: Productivity

If debt is the constraint, then productivity is the engine. There is only one sustainable way to offset high debt levels: producing more output with fewer inputs. Productivity growth has historically been the foundation of rising living standards, tending to come in waves, on the back of technological breakthroughs and when they arrive, they can change the macro picture faster than people expect.

It allows economies to absorb higher levels of debt without collapse, not through austerity, but through real income growth. It is the only true win-win outcome.

The AI Opportunity

Artificial intelligence offers the potential for a new wave of productivity, one that could be faster and more far-reaching than anything seen before. This is not just another technology cycle. AI is a general-purpose tool that affects decision-making, design, logistics, research, and capital allocation simultaneously.

The question is not whether an AI-driven productivity boom will emerge. It is whether it will arrive quickly enough to counterbalance the growing pressures within the financial system. In many ways, this has become a race.

The Investor’s Dilemma

History shows that transformative technological shifts are extremely difficult to invest in directly. During the early days of the automobile industry, thousands of companies emerged. Only a small number ultimately survived. The lesson is clear: the direction of change may be obvious, but the winners rarely are. Instead of trying to pick specific winners, it is often more useful to focus on what becomes obsolete and what becomes scarce.

As digital capabilities expand, costs in the virtual world fall. Meanwhile, constraints shift toward the physical world: energy, infrastructure, materials, and skilled labour. These constraints are structural, not cyclical. And where there is scarcity, there is pricing power.

Creating More from Less

In a world defined by rising debt and persistent debasement, there is only one true path forward: productivity. Over time, capital will flow to the people, businesses, and systems that can consistently deliver more with less.

At Capital International, this principle sits at the heart of our investment philosophy. We believe the companies best positioned for long-term success are those that can expand output while continually improving efficiency, driving growth without a proportional increase in inputs.

Our strategies are designed to give investors access to these highly productive assets, companies we believe are capable of compounding value by doing more with less.

To learn more about our asset management services, please get in touch with our team.

The views, thoughts and opinions expressed within this article are those of the author, and not those of Capital International Group Limited (Group) and/or any of its subsidiary companies and as such are neither given nor endorsed by the Group or any company within the Group. Information in this article does not constitute investment advice or an offer or an invitation by or on behalf of any company within the Group to buy or sell any product or security or to make a bank deposit. Any reference to past performance is not necessarily a guide to the future. The value of investments may go down as well as up and may be adversely affected by currency fluctuations. The Group, its subsidiary companies, clients, and officers may have a position in, or engage in transactions in any of the investments mentioned. Opinions constitute views as at the date of issue thereof and are subject to change.

Regulated investment activities are undertaken by Capital International Group Limited's licensed subsidiary companies. Capital International Limited and Capital Financial Markets Limited are licensed by the Isle of Man Financial Services Authority. Capital International Limited is a member of the London Stock Exchange. Capital International, Capital International Asset Management, and Capital International Investment Platform are trading names of Capital International Limited. Capital International is a trading name of Capital Financial Markets Limited. CILSA Investments (Pty) Ltd (FSP No. 44894) is authorised by the Financial Sector Conduct Authority in South Africa. Capital International (Jersey) Limited is regulated by the Jersey Financial Services Commission. Capital International and Capital International Asset Management are trading names of Capital International (Jersey) Limited. Capital International (Jersey) Limited (FSP No. 51164) is authorised by the Financial Sector Conduct Authority in South Africa.