Emerging Market Debt Final

Sovereign Default Risk in BRIC Countries Part 2

Following my recent introduction to the Sovereign debt I will herein focus on Brazil, Russia, India and China also known as the BRIC countries. In the early 2000’s these countries changed their political systems and embraced global capitalism to some degree. Goldman Sachs predicted that China and India, would become the dominant global suppliers of manufactured goods and services, while Brazil and Russia will become dominant as suppliers of raw material. I will unpack the subject of contagion, which references not only academic data but also my thoughts on the trade war.

What determines the ability of developing countries to issue bonds and gain access to international capital markets?

Generally the richer and larger a country is, the more likely it is able to access credit markets. The perceived market quality of a country is a key driver in market access. Accordingly, countries more vulnerable to shocks are less likely to be able to tap these international markets. This extends to countries like Venezuela where, according to the World Bank, since 2012, 96% of the country’s exports and nearly half of its fiscal revenue relied on oil production. The impact of falling oil prices is a perfect example of a shock caused by the concentration of risk.

What we have found?

Not all Emerging market countries are equal, although Russia and Brazil are both primarily commodity driven economies exhibiting a moderate correlation (0.518). Russia and China exhibit strong correlation (0.814). They also have the strongest correlation to the VIX meaning they are more driven by global indicators. While Brazil and India do not seem to be correlated to global indicators. Not only are Russia and China correlated but Russia seems to be viewed historically has the riskiest of BRIC countries and China the least risky. At the moment however the default risk of Russia is much lower than that of Brazil. Russia seems to go through short periods of extremely high volatility which ultimately distorts the default risk of the country.

BRIC countries default risk

To compare the sovereign rates of the BRIC countries to those of the developed economies I have decided to use the Credit Default Swaps (CDS). CDS is a type of swap which is designed to transfer credit exposure of fixed income securities. This in effect is insurance on the bond and gives markets perceived risk on the countries underlying those bonds. These derivatives make it easier to see causal relationships between countries; which can be useful not only in portfolio construction but also in predicting contagion in sovereign debt markets. I have used a 5-year senior CDS index, which tends to be the benchmark and the most actively traded and quoted.

In the aftermath of the 2007-2009 global financial crisis, most of the emerging markets managed to avoid a full-fledged sovereign debt crisis (in contrast to European countries). Up until fairly recently, BRIC’s have fared relatively well during developed market crises. During the Eurozone financial turmoil for example, the BRIC’s sovereign debt held up pretty well while their stock markets were hit strongly during this period. The two most important global variables that are believed to have the most significant impact are the VIX index and TED spread. The VIX is a measure of volatility in the markets. A higher VIX is often thought to be a risk off stance in equity markets. The TED spread is the difference between the interest rate on short-term US government debt and the interest rate on the interbank loans. It is also a measurement of risk but more specifically ‘credit risk’. This is because U.S T-bills are considered risk free, as the TED rate increase the default risk of interbank is considered to be increasing. This rate has been around 36 bps year to date but the highest (2008) was 450 bps which goes some way to understanding the type of pressure banks were under during the financial crisis.

When looking at CDS or any other indicator of Sovereign default risk, it is important to make the distinction between contagion and interdependence. For example during the Eurozone’s sovereign crisis, Germany’s CDS prices also rose, however this was not contagion, it was merely a reflection of the interdependence. Whereas core economies have greater ability to cause contagion international. Global factors such as the VIX index or TED spread do not significantly influence the EU core CDS prices but these economies are more sensitive to intra-EU and financial market variables such as the dynamics of the DAX index. Unlike the Eurozone, the Emerging Market CDS spreads are linked to global indicators. For example, the VIX index and TED spreads are significant indicators for Latin American CDS prices, including Brazil. This also applies to the greater emerging market CDS prices. Ultimately, the global and regional risk premia contribution is much more important in emerging markets than in country-specific macroeconomic variables or than the ratings from Standard & Poor’s, Fitch and Moody’s. An investigation into the determinants of daily CDS spread for twelve emerging markets from different regions was conducted over the period of 2002-2011. They found that risk premia embedded in global indicators such as the VIX index, US bonds and equity returns outperformed country-specific risk.

Core economies have a greater ability to cause contagion internationally, which is perhaps a product of globalisation. Interesting though is the fact that the EU does not buck the same trend (with global factors such as the VIX index or TED spread not influencing the EU core CDS prices significantly). These economies seem to have a more localised risk. This leads the EU to have risk spill-over from peripheral economies inside the EU (something that Mario Draghi would probably not like to hear). Nevertheless, the overall impact of these peripheral economies is relatively low.

Brazil

While Latin American countries experience financial crises associated with large fiscal imbalances, it has been noted that the subsequent inflation acts more like an instrument of fiscal policy in these countries, compared to that of developed. For example, the crisis in Argentina (2001-2002) was a triple crisis, as it failed to maintain its peg with the USD. The banking system became insolvent and the government defaulted on its payments. With the Brazilian Real down 22% YTD by September, it appeared susceptible to the same forces of contagion which were impacting other EM countries like Turkey and Argentina. Brazil’s reliance on external debt is relatively low which makes it somewhat less vulnerable to external forces. We can see this to a certain degree in the correlation matrix below whereby Brazil exhibits a very low correlation to the TED spread and VIX index.

Russia

While most academic research has focused on Latin America and China. I was able to source some journals, which focused on Russia, which is particularly timely, as the country came under scrutiny earlier in the year. The serious political risk the country has been facing since 2014-2015 provides a localised risk premium. Geopolitics, however, are not the only variable effecting the value of Russian CDS. Similarities between Venezuelan and Russian sovereign credit risk can be made with both countries exhibiting correlation with oil prices.

The most important factors for Russian sovereign credit risk are the VIX index, oil prices, credit rating agencies and TED spreads. In graph 2 below it’s easy to see the correlation between the variables.

Graph 1 (Shows Russia’s and Brazil’s CDS, TED and VIX from January 2017 to October 2018)

In graph 1 it’s hard to see any correlation between either the VIX or Ted spread and the CDS of Russia and Brazil. However, there looks to be a reasonable correlation between the two countries. Even though Russia’s CDS might not have been effected by global factors they still cancelled their weekly regular sale of ruble government bonds twice in a row back in September. Citing the possibility of deeper US sanctions and EM flight as reasons. This is the first time they have done this since the oil price plunged in 2015. Russia borrowing costs are now significantly higher, nearer the highest level they have been in two years.

Graph 2 (Shows Russia’s CDS, TED and VIX from January 2007 to January 2010)

China

China’s CDS price is heavily dependent on global indicators and country-specific risks e.g. China’s stock market. This dependence on global indicators has, arguably, become more pronounced over the years, as the country becomes more integrated with capital markets and a more significant global player. Fender et al. (2012), showed that since 2007 the importance of global versus local factors has increased. Ismailescu and Kazemi (2010) find that positive credit rating drive the spreads shortly after the announcement but CDS markets themselves anticipate the downgrade, so CDS spreads could be used as a negative credit downgrade indicator.

Graph 3 (Shows China’s CDS, TED and VIX from January 2005 to October 2018)

China and Russia exhibited the highest correlation to global factors. Which in China’s case I believe makes a lot of sense as they have a fairly large world share of GDP at 18.72%, while the other the three BRIC countries make up only 13.27%. These figures were sourced from the IMF.

Graph 4 (Shows China’s CDS, TED and VIX from January 2015 to October 2018)

Over the period of January 2005 to October 2018, I ran a pearson correlation and tested for 2 tail significance at the 95%. I also ran some descriptive characteristics on the data to see what the distribution and standard deviation of the data was. Unfortunately the data for India was only available from after October 2013 so the sample size was limited. After running some stats on the CDS for the BRIC countries (and also for the TED spread and VIX index); some interesting results emerged. Whilst I expected Brazil and Russia to have a strong correlation, due to the reliance on commodities, the strongest correlation was between China and Russia (0.814). This is rather strange, as one would expect an inverse relationship between commodity prices and the margins on goods. Russia also has the highest standard deviation by far at 138.91 and the largest range with CDS spread being just 36.9 in June 2007 going all the way up to 1113.4 in October 2008.

As one might expect, the kurtosis in Russia is extremely positive at 7.4 this is 10 times that of Brazil and India. This means that the Russian data has extremely heavy tails. Something which is fairly interesting, as the Russia mean is just below that of Brazil.

In summary, the findings point to a limited role of domestic macroeconomic factors in curbing sovereign debt crises. I believe that credit rating agencies are probably laggards in predicting sovereign default. Emerging market debt instruments will likely become more important in portfolio construction in the future, as these countries become more dominant global players. I also believe that more research needs to be conducted around the topic of defaults of emerging market countries particularly the BRIC countries as they are the most important of the emerging market countries. I have only come across a couple of databases on political risks, one being the International Country Risk Guide. The significance on indicators which evaluate political risk factors in credit markets would be invaluable.

Graph 5 (Shows CDS of the BRIC countries from January 2005 to October 2018)

Statistical table

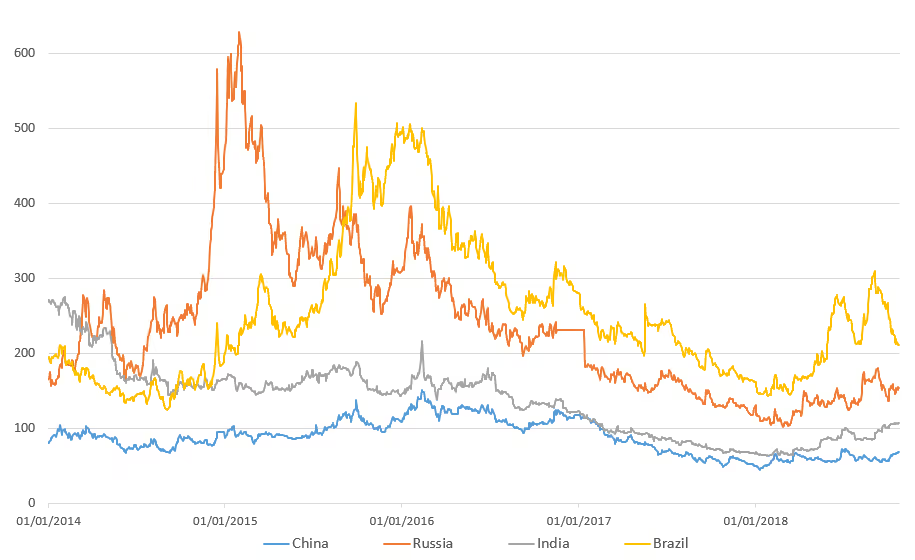

Graph 6 (shows the CDS of the BRIC countries from January 2014 to October 2018)

Disclaimer: The views thoughts and opinions expressed within this article are those of the author, and not those of any company within the Capital International Group (CIG) and as such are neither given nor endorsed by CIG. Information in this article does not constitute investment advice or an offer or an invitation by or on behalf of any company within the Capital International Group of companies to buy or sell any product or security.