G7 2030 Nature Compact

During Q2 we saw a G7 summit that strengthened commitments to the Paris Agreement and resulted in a renewed pledge to halt and reverse biodiversity loss by 2030.

Whilst the commitments made at the summit might not have been as strong as activists would have wished, the direction of travel towards COP26 (Convention on Climate Change) and COP15 (Convention on Biological Diversity) is now clearly mapped out in the G7 2030 Nature Compact.

The past quarter has seen some significant polemic action impacting both companies and governments around the world.

In May, climate change activists won a monumental legal victory in the Dutch courts that compels Royal Dutch Shell to reduce its greenhouse gas emissions by 45% by 2030 from 2019 levels (Milieudefensie v Shell 2021).

In June we saw France’s highest administrative council, the Conseil d’Etat, order the French Government to take additional measures by the 31st March 2022 to enact climate policies as part of their commitment to reducing greenhouse gases by 40% of their 1990 levels by 2030.

Both of these cases highlight the increasing pressure on businesses and governments to implement meaningful change. Our expectation is that implementation of climate change legislation will continue to increase, forcing polluters to adapt their business models or face financial and regulatory penalties.

As an ESG investment manager, we review the progress that companies are making through disclosures contained in their sustainability reports; whilst reporting standards have improved, there is long way to travel if the global economy is going to meet the Paris Agreement goal of limiting global warming to below 1.5 degrees Celsius compared to pre-industrial levels.

In the wake of the G7 communique, we have started to see companies across many sectors issue statements committing to ‘Net Positive Biodiversity Impact’ by 2030. As with companies that committed early to climate change initiatives, those that are leading from a Biodiversity perspective are, in our view, best positioned to manage biodiversity risks.

In June we hosted a biodiversity focused webinar for trustees and institutional clients; you are welcome to view the content.

Inflation and Conflagration

While inflation might be transitory, it is abundantly clear that the climate and biodiversity crises are not.

Heat Domes, drought and plagues of grasshoppers in the north-west of North America have created conditions not seen since the 1930’s when the United States suffered severe dust storms and crop failure.

The map below shows the intensity and impact of the current severe heat wave, with the United States Department of Agriculture declaring multiple states of emergency across California, Wisconsin, Illinois, North Dakota, Idaho and Utah on the 6th July 2021.

Concurrently, the drought has created ideal conditions for massive swarms of grasshoppers to proliferate across the mid-west with the economic cost estimated at $9 billion according to the USDA.

Why are we commenting on heat-domes and grasshoppers?

Because it shines a light on the global risks that climate change and biodiversity loss pose, and it demonstrates how close we are to an agricultural crisis with soft commodity inflation and food shortages. Whilst we have highlighted the US in this review, the impacts are being played out across Europe, Asia and Africa.

Wildfires are once again raging across California and further north across Oregon, which has seen all-time record temperatures recorded (48 degrees Celsius at Canby, north-western Oregon).

In Douglas County, Washington for example the Batterman fire has burnt over 7,900 acres of land.

On a positive note, we are seeing increasing opportunities within Agricultural Technology, Precision Farming and Yield Enhancement, with companies focused on finding more sustainable, profitable and future-proof farming practices.

Within Fusion ESG we have added the Sarasin Food and Agriculture Opportunities Fund to bolster our existing position in Pictet Nutrition, taking our Sustainable Agriculture thematic weighting to 6.80%.

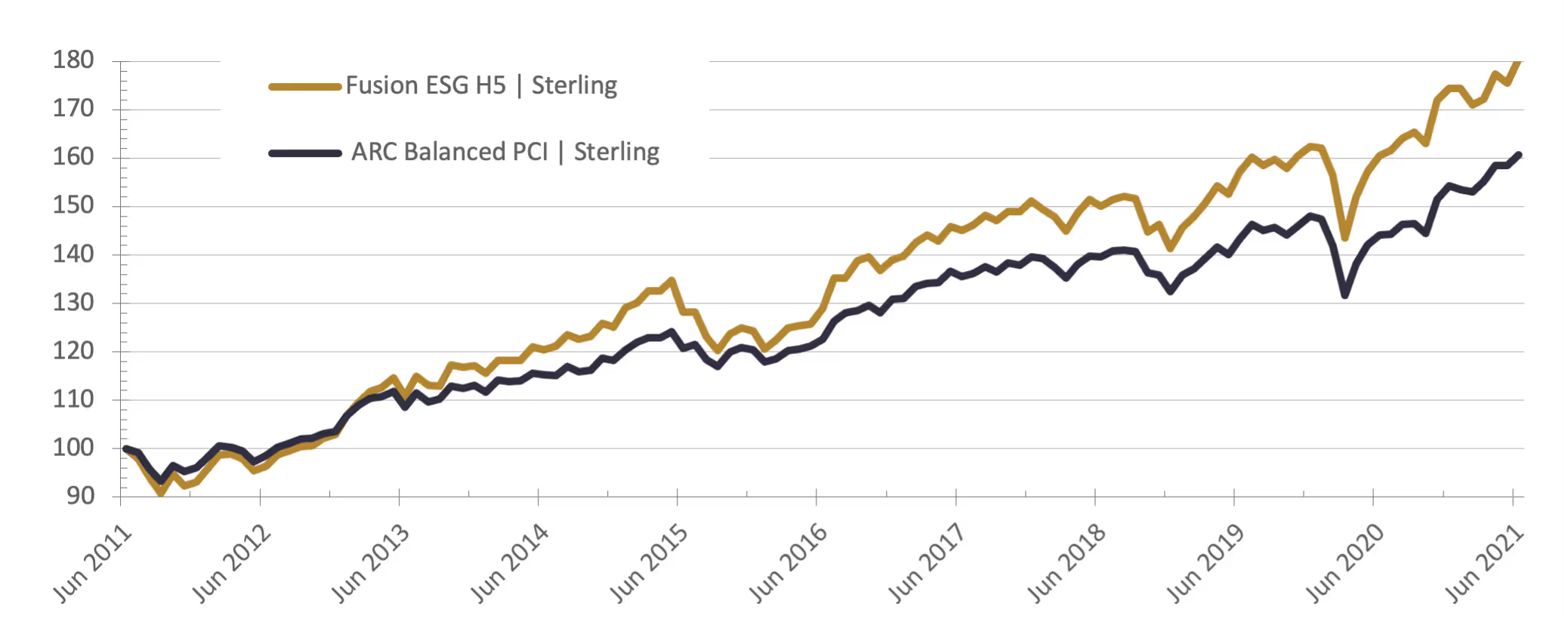

Fusion ESG Performance

Performance over Q2 for our moderate risk Fusion ESG GBP H5 strategy was 4.84% compared to the ARC Balanced PCI benchmark return of 3.53%. Over 12 months, Fusion ESG GBP H5 has returned 12.50% compared to the ARC Balanced PCI benchmark return of 11.51%.