“America first” might be true in America, but in the Global base metals and Steel markets it’s very clear that China holds the trump card. If China is not the biggest global miner in a particular base metal, they are the single biggest importer and refiner of most base metals. Trump might be able to impose US sanctions on Iran, however when it comes to the trade wars in Base metals and Steel, China will not easily “Panda” to the US. It was relatively easy for the US to impose sanctions on Iran because the US is no longer as dependent on OPEC and IRAN for oil as they used to be.

Volatility in Base metals

Base metal prices have certainly not been immune to volatility. All base metals have gone backwards in 2018. Zinc and Lead were down at one point by 20% whereas the broader commodities, represented by the CRB index, were down by only a 1%. The CRB commodity index was created in 1957 to provide a dynamic representation of broad trends in overall commodity prices. Copper, which is recognized as a lead base metal, has fallen less in 2018 and is down by 14%.

The weakness in base metal prices was as a result of the uncertainty around global economic growth and more specifically Chinese growth. Trade wars have had an effect on sentiment. Resulting, not only in a drop in the base metals prices, but inventory levels as well. During October, LME inventories reached their lowest levels for 2018 (The LME is the London Metals Exchange).

The sharp drop during 2018 in base metals could be an overreaction. This can be likened to US market drop in 2008 where the US S&P500 was down by 56% to a low in 2009 (See chart below). 10 years later the S&P500 was up nearly 289% from its lows (70% from the previous highs in 2007/2008). The difference between base metals now and what happen to the S&P500 in 2008/2009 was that there were significant underlying debt problems behind the falling market. The prices in base metals this year have fallen sharply in anticipation of much lower growth, however global growth is only showing signs of slowing and not entering a recession. A strong case can be made that base metal prices have fallen too low and accordingly are showing attractive long-term value at current levels. Exiting the S&P500 prematurely in 2009 would have not only locked in large capital losses but investors would have missed the returns over the following 10 years.

Just how big is China?

The overall market size of Base metals and Steel based on approximate annual production is detailed below.

The value of annual global steel production dwarfs the base metal market. In fact the value of annual steel production is larger than the value of all other base metals production combined. The chart below shows that China produces more than 50% of global steel which is 8 times more than its closest competitor Japan.

China produces 36% of global refined copper.

The 2nd biggest base metal after Copper is Aluminium. While China is not the largest miner of Aluminium (Bauxite), they produce 54% of the global refined Aluminium.

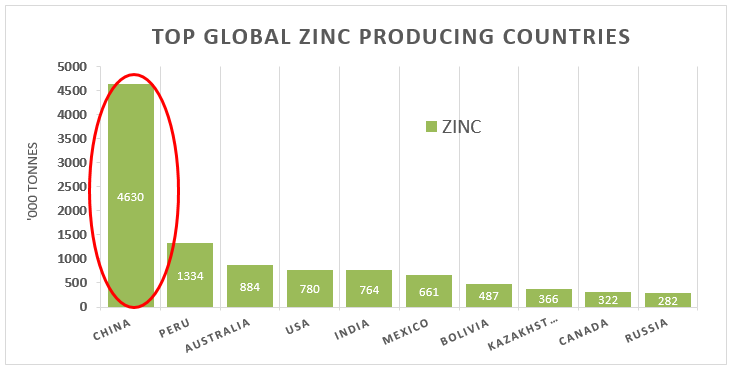

Moving onto Zinc, China is a clear leader, producing 40% of global Zinc.

Once again China is the top producer of Nickel making up 30% of the global market. 50% of Zinc production is used in galvanizing Steel and 67% Nickel is used in Stainless Steel.

There is a noticeable trend in base metals and its no surprise that the remaining base metals, Tin and Lead, are dominated by China. China produce 50% of global Lead and 30% of global Tin. 91% of China steel production is consumed internally. In contrast the US is the biggest importer of global Steel and their biggest import partner is Canada and not China. China only accounts for around 2% of US steel imports. Lower growth in China could mean significantly more Steel available on the global market. This would put downward pressure on steel prices that would hurt not only the US steel trading partners but the domestic US steel industry. The 25% Steel tariffs imposed by the US on China earlier this year is a reaction to the threat that China poses to the steel industry if they were to dump excess steel in the event of a slowdown in China. Over the last 7-8 years the most significant change in the oil market was the US drive for self-sufficiency in oil supply. The US would like nothing more than to exercise the same level of independence they enjoy in oil supply in the steel market. Unfortunately, for the US, China remains dominant in Steel and in most base metals and will not easily “panda” to trump.

Graphs source: Reuters

Disclaimer: The views thoughts and opinions expressed within this article are those of the author, and not those of any company within the Capital International Group (CIG) and as such are neither given nor endorsed by CIG. Information in this article does not constitute investment advice or an offer or an invitation by or on behalf of any company within the Capital International Group of companies to buy or sell any product or security.