Much has been written in recent years about ethical investments, impact investing, socially responsible investments and ESG (Environmental, Social and Governance) strategies.

This article is not going recite the definitions of ESG or try to provide an exhaustive list of exclusion or inclusion criteria, as most market participants have a base level awareness of these factors. ESG investing is by nature, broad in scope and investor views are spread across a wide spectrum.

We will focus instead on the state in which we find the global economy and financial markets from an ESG investing perspective.

Having designed, developed and managed a sustainable agriculture fund with my father from 2010 to 2013, the question I have been contemplating recently is whether market participants are now fully embracing ethical investments and if the economic and societal impact of COVID-19 might precipitate a paradigm shift in investment management towards a more sustainable model or, whether as experienced in the wake of the Global Financial Crisis of 2007-9, the momentum behind ESG will evaporate as multi-national businesses and investors focus on survival.

Will we all be driving EV’s in the near future or will we revert to fossil fuels?

We are not there yet. The world is still awash with powerful industrialist and climate change deniers both in finance and government. It is in many ways a gradual generational shift with COVID-19 being one in a long line of events that highlights global wealth and health inequalities.

Sustainability and capitalism are not ontological dualisms (nature vs nurture or good vs evil), they can co-exist and thrive. Divisive as some may find him, Elon Musk is a remarkable example of this hybridisation of sustainability, capital growth and progress (Tesla is trading at $956.50 as at time of writing having started the year at $430).

ESG portfolios have for many years been regarded as a niche offering to clients. Investment managers have debated and used perceived wisdom to assess that this type of portfolio will underperform due the exclusion of significant sectors of the market and the limitations a smaller universe would have on diversification.

Conversations and considerations have evolved and the underperformance myth can to a large extent now be debunked.

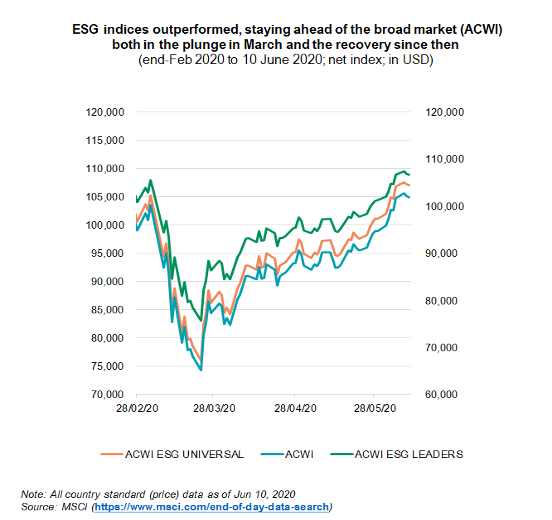

The graph illustrates how the MSCI ACWI ESG Universal Index and ESG Leaders Index have (out)performed relative to the ACWI through both the rapid fall in equity markets during Q1 and the remarkable recovery that has taken place during Q2.

The positive performance comparison though is not just a short-term phenomenon.

Over the longer-term the ACWI ESG Universal Index has an annualised historical 10-year return of 6.84% versus 6.38% for the ACWI Index.

Exclusion criteria have been used for decades. They remain however largely subjective (there is no algorithm for determining whether a stock is inherently ethical). To impartially and quantitatively screen a stock and thereby gauge its appropriateness for an ESG portfolio, investment managers, Capital International included, can assess and attribute ESG scores as part of their equity research. These scores are based on analysis of corporate activities from an environmental, social and governance perspective.

This approach helps to put a quantitative process in place to establish a view on whether an asset meets the managers criteria or whether the asset should be excluded from a portfolio with an ESG mandate.

This approach is still prone to qualitative judgement calls, for example should BP be included in an ESG portfolio?

On the surface it would seem an automatic exclusion based on the fact it profits from fossil fuels. However, BP is actively engaged in renewable energy production, scores highly on inclusivity and diversity perspective and has a target of being net carbon zero by 2050.

But have BP really changed their thinking? Not if their annual shareholders meeting in April is anything to go by:

‘Oil giant BP today signalled it would press on with a controversial Canadian tar sands project despite facing a showdown with environmental campaigners and shareholders.’ - Holly Williams in The Independent

Exclusion criteria are broad in their scope and we do not have time to unpack each subject here, but for those to whom ESG investing is a new consideration, the typical exclusions are companies that are carbon intensive, have poor employment practices, have abused human rights, have poor animal welfare records or companies that operate in and profit from Alcohol, Tobacco, Adult Entertainment, Gambling, Nuclear power or Armaments.

As investment professionals we are indoctrinated to take emotions out of investment decision making. Within the context of ESG, this philosophy is often tested. It is important for all investors to remain rational with their investment decision making; whether you are an institution or a private client, seeking guidance from your investment manager with regard to ESG considerations should be as important as determining your risk profile and return expectations in shaping your overall investment objectives.

Investment managers and market participants are imperfect human decision makers. As such, you can expect risks, failures and losses in an ESG portfolio as much as in a standard portfolio. There are perhaps more potential pitfalls in ESG investing, with an eagerness to positively contribute to a ‘good’ investment sometimes leading to naïve investment decision making.

It is prudent to avoid illiquid and opaque or poorly defined structured investments. As Nasim Taleb wisely notes in his book Antifragile: ‘Any strategy that includes potential ruin should be avoided.’

There are also many well-founded but often financially unviable projects seeking private client, institutional and family office funding. Sometimes, no matter how laudable the cause, investors are wiser to offer support in non-financial ways by giving their time or sharing their knowledge, for example. Try to avoid conflating ESG investing with philanthropy. If you want to give, then give. If you want to profit, endeavour to do so in a way that befits your own ESG objectives and financial landscape.

In the final section of this article we will briefly consider ESG investments from a legacy perspective.

A trustee and friend that I’ve worked with over the years often starts their client discussions by asking what legacy they wish to leave to their beneficiaries and future generations. Sustainability and ESG is becoming a key component of that conversation. I do wonder what wealthy 5th or 6th generation decedents of imperialists think of their ancestors’ original source of wealth. The age of empire brought with it some of the most vulgar profits at a tremendous long-term cost to society and the environment.

How will future generations view the investment decisions made by today’s stewards of family wealth?

I sometimes consider whether my daughter would inherit an ESG debt or benefit from the investment decisions I make for my own small portfolio. Every asset in your portfolio should be able to stand up to your own conscience and integrity test. Your portfolio is, in some ways, a reflection of personally held world views. You should be comfortable with the investments you hold from an ethical perspective and look to allocate to themes that resonate with your ESG objectives.

The decisions that investors make now will echo through history. In 80- or 100-years’ time, will our great-grandchildren look back in abhorrence that we as investors in 2020 were still allocating to non-ESG assets when we had knowledge that these choices would be to the detriment of the planet and humanity?

As we move into the second half of 2020, the world is still in the midst of a pandemic with the IMF forecasting a $12.5 trillion cumulative output loss with the global economy contracting by 4.9% this year.

The IMF are also forecasting global growth of 5.4% in 2021. How and when the economy emerges from the pandemic is still unknown; perhaps there should be cause for hope that companies embracing ESG will be at the forefront of a post-COVID-19 global economy.

I’ll leave readers with a rhetorical question: What does sustainability mean to you and what are your ESG objectives? Has COVID-19 changed the way you think about investing? It remains a subjective matter and one that clients should be determining when they invest capital. In my humble view, it is just as important as deciding your wider investment objectives, attitude to risk and your investment horizon.

Undeniably the world and our island have changed in 2020. Our approach to portfolio management has altered too, with sustainability being at the forefront of our thinking. Only time will tell whether the grubby fat investment caterpillar is finally ready to pupate into an ESG butterfly.